Tax preparation checklist sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail with casual formal language style and brimming with originality from the outset.

As we delve into the intricacies of tax planning, preparation, optimization, and returns, let’s explore how these key elements can shape your financial landscape.

Tax Planning

Tax planning is a crucial aspect of financial management that involves strategizing to minimize tax liabilities and maximize savings. By carefully planning your taxes, you can ensure that you are taking advantage of all available deductions, credits, and exemptions to reduce the amount of taxes you owe.

Importance of Tax Planning

Tax planning is essential for individuals and businesses to effectively manage their finances and minimize tax liabilities. It allows individuals to make informed decisions about their investments, retirement accounts, and other financial matters to optimize their tax situation. For businesses, tax planning helps in maximizing profits by identifying opportunities for tax savings and complying with tax laws to avoid penalties.

- Regularly review and adjust your tax withholding to avoid overpaying or underpaying taxes.

- Maximize contributions to retirement accounts to reduce taxable income.

- Take advantage of tax-deferred investment accounts like IRAs and 401(k)s.

- Utilize tax credits for education expenses, energy-efficient home improvements, and other eligible expenses.

- Consider gifting appreciated assets to reduce capital gains taxes.

Minimizing Tax Liabilities for Businesses

Tax planning is essential for businesses to minimize tax liabilities and maximize profits. By strategically planning their finances, businesses can take advantage of deductions, credits, and exemptions to reduce their tax burden and improve their bottom line.

By carefully structuring business transactions, utilizing tax credits and deductions, and staying compliant with tax laws, businesses can minimize their tax liabilities and ensure long-term financial success.

- Implement tax-efficient business structures to reduce tax obligations.

- Take advantage of tax credits for research and development, energy efficiency, and other eligible activities.

- Keep detailed records of expenses and deductions to accurately report taxable income.

- Consult with tax professionals to identify tax-saving opportunities and ensure compliance with tax laws.

Tax Preparation

When it comes to tax preparation for individuals, there are several key steps to follow to ensure accuracy and compliance with tax laws.

Self-Employed Individuals vs. Employees

Self-employed individuals and employees have different tax preparation processes due to their unique financial circumstances.

- Self-employed individuals need to keep detailed records of their income and expenses throughout the year to accurately report their earnings and deductions.

- Employees, on the other hand, receive a Form W-2 from their employer, which summarizes their income, taxes withheld, and other relevant information.

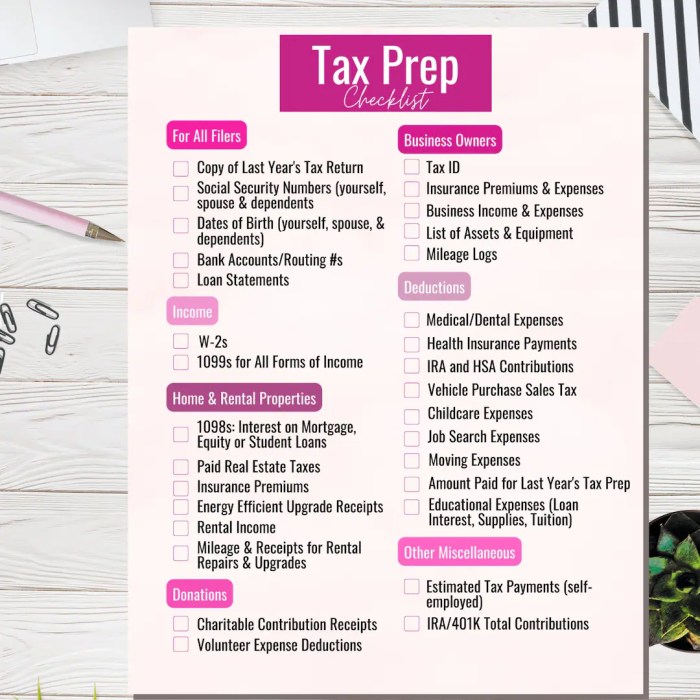

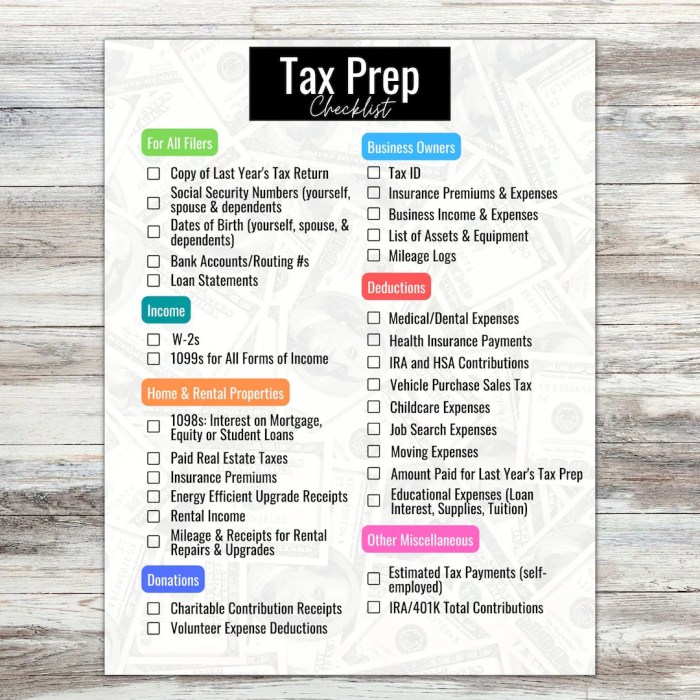

Organizing Documents for Efficient Tax Preparation

Organizing your documents is crucial for a smooth tax preparation process. Here are some tips to help you stay organized:

- Keep all important tax documents in one central location, such as a folder or a digital file.

- Separate your documents by category, such as income statements, deductions, and receipts.

- Use an organizer or checklist to ensure you have all the necessary documents before starting your tax return.

- Consider using tax preparation software or hiring a professional to assist you with complex tax situations.

Tax Optimization

Tax optimization refers to the strategic planning and use of legal methods to minimize tax liabilities and maximize tax efficiency. By optimizing taxes, individuals and businesses can take advantage of deductions, credits, and other tax-saving opportunities to reduce their overall tax burden.

Common Tax Optimization Techniques

- Utilizing tax-deferred accounts such as 401(k) or IRA to save for retirement and reduce taxable income.

- Claiming all eligible deductions, such as mortgage interest, medical expenses, and charitable contributions.

- Timing income and expenses to take advantage of lower tax rates in certain years.

- Harvesting investment losses to offset capital gains and reduce taxable income.

- Maximizing tax credits, such as the Earned Income Tax Credit or Child Tax Credit, to reduce tax liability dollar-for-dollar.

Tax Optimization for Businesses

Businesses can optimize their taxes by implementing various strategies that align with their financial goals and operations.

- Choosing the right business structure, such as an S Corporation or Limited Liability Company, to minimize tax liabilities.

- Taking advantage of tax deductions for business expenses, including salaries, rent, utilities, and supplies.

- Utilizing tax credits for research and development, hiring employees from certain groups, or investing in renewable energy.

- Strategic tax planning to minimize the impact of taxes on business transactions, mergers, acquisitions, and expansions.

- Regularly reviewing and updating tax strategies to adapt to changes in tax laws and regulations.

Tax Returns

When it comes to filing tax returns, it is essential to understand the process and deadlines involved to avoid any penalties or issues with the tax authorities. Filing tax returns is the process of submitting your financial information to the government to determine your tax liability or potential refund. It is mandatory for individuals and businesses to file their tax returns annually.

Essential Documents for Filing Tax Returns

- W-2 forms: These forms provide information on your wages, tips, and other compensation received from your employer.

- 1099 forms: These forms report income from freelance work, investments, or other sources.

- Receipts for deductible expenses: Keep records of expenses such as medical bills, charitable donations, and business expenses that can be deducted from your taxable income.

- Proof of retirement account contributions: Documents showing contributions to IRAs, 401(k)s, or other retirement accounts can help reduce your taxable income.

- Social Security numbers for yourself, spouse, and dependents: Ensure you have the correct social security numbers for all individuals included in your tax return.

Implications of Errors in Tax Returns and How to Rectify Them

Filing incorrect information on your tax return can lead to penalties, interest charges, or even audits by the tax authorities. If you realize you have made an error on your tax return, it is important to rectify it as soon as possible. You can file an amended tax return to correct any mistakes or omissions. It is crucial to provide accurate information to avoid any legal or financial consequences.

In conclusion, the Tax preparation checklist serves as a fundamental tool in navigating the complex terrain of tax management, ensuring a seamless and efficient process for individuals and businesses alike.

FAQ Overview

What are some common tax planning strategies for individuals?

Some common tax planning strategies for individuals include maximizing retirement contributions, taking advantage of tax credits, and proper income deferral.

How can businesses optimize their taxes through strategic planning?

Businesses can optimize their taxes through strategic planning by conducting regular tax audits, taking advantage of deductions, and structuring transactions efficiently.